From Dr. Housing Bubble (link here):

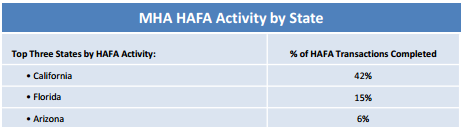

The bailout of the banking industry was under the pretense that it would help the average homeowner. What is interesting is that we are now subsidizing the foreclosure process for many of these homes to be sold to investors. In California, roughly one-third of home sales for the last couple of years have gone to investors. HAFA (Home Affordable Alternative Program) has made the process of selling distressed homes much easier via short-sales and deed-in-lieu of foreclosure. Take a look at where most of this has occurred:

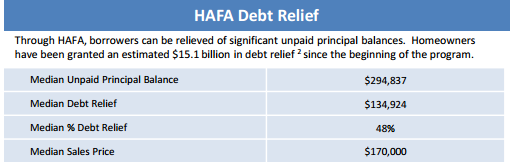

42 percent of all HAFA activity has occurred in California. This has not come at a low price:

What is troubling about this is that many regular homeowners would like to buy these homes if they were actually on the market. In fact, many would pay fair market value if these homes made it to inventory in a more normal fashion instead of going through the labyrinth of government programs and bank alternative-accounting standards. Instead, these large cuts in balances are feeding into the investor frenzy. The end result is a dragged out foreclosure process and the market suffers with a lack of inventory.

Going to any open house in Southern California during a sunny weekend will make you think that the entire housing market is on fire and that the homeownership rate must be going up. Obviously with all these buyers, the rate must be going up. Right? Well, it isn’t because a large number of these buyers will be absentee buyers or will flip the house shortly. Another bigger reason comes from the lack of supply. The maddening crowds are simply hungry investors and regular buyers trying to out-bid each other for the limited supply of homes on the market. Low rates are adding fuel to this mania but the homeownership rate continues to decline.

What higher housing prices and lower ownership rates means is that the benefits are going to fewer and fewer of those who merely want to exploit housing as a speculative asset market rather than a place to live. These are the folks who have benefited directly from bank bailouts and easy monetary policy from the Federal Reserve. The upshot is that the wealth gap between the haves and the have-nots is widening as a direct result of government policy. Is this what we voted for?

(Note: I should add that there is nothing wrong with investors making their bets in a free housing market, but the government shouldn’t be tipping the scales in their favor. The price volatility of an asset market increases its attraction for speculators by creating a greater potential for quick profits. This is the mistake we’ve made with an asset so essential as homes. Instead of secure homeowners to support a growing economy, we’ve created lots of winners and losers, all leveraged with unsustainable debt.)