1971’s break of the gold-pegged US$ to become a fiat-based currency has been a consistent thread throughout the life of this blog. Here is a compendium of charts illustrating the macroeconomic effects we’ve been living through for the past 50 years:

The title of this essay alludes to the card game of Bridge. My parents played Bridge; my grandparents played Bridge; I have no clue how to play Bridge. I suppose it’s becoming a lost art, kind of like playing piano in the parlor. Forsaken pianos have become a nice piece of furniture in a well-appointed house (disclosure: I have a grand piano, I love it, I play it, but I’m no pianist). One thing I did find fascinating about Bridge are those terms “trump” and “no trump.” I have no idea what they mean in Bridge, but in the political context I do, and it’s not good.

I’m one of those many squeezed between the Trump and No-Trump political tribes. I often end up arguing points of difference with both. Back in 2016 I was a No-Trumper, mostly because I thought he was completely inexperienced as a political leader and suspected his campaign was mostly a publicity stunt. I was no fan of Hillary Clinton either and voted for neither. I was as surprised as anyone when Trump actually won. (And yes, he did win. The national voting data showed that Trump won convincingly across the broad landscape of the country. Russian bot interference was not in any way determinant.)

However, I found the craziness that ensued after Trump’s election rather troubling. As a long-time student of US politics, I knew Trump was a symptom, not the cause of our national political dysfunction. But the No-Trumpers had convinced themselves that he was the cause of all our national chaos and therefore needed to be removed at all costs. I suspect this thinking follows from the Great Man (Person?) perspective on history. The prime example of this school of thought is that if there had been no Hitler there would have been no Second World War and no Holocaust. I have never found this approach a convincing way of understanding history. Did Hitler create Mussolini? Stalin? Mao? The Japanese military machine? Single personalities certainly do shape the contours of history, but I truly doubt they are the singular or dominant cause of what transpires on a grand scale. If Putin or Xi had not arisen, someone similar would have taken control of these authoritarian regimes.

The past six years of national political disorder promoted by the No-Trump left and right has convinced me that perhaps we need to continue to disrupt the political status-quo. After all, who were the great disrupters in 2016? Not Hillary Clinton or Jeb Bush. No, the disrupters were Bernie Sanders and Donald Trump. The DNC kneecapped Sanders in the primaries, so we the people elected the Chief Disrupter. And who were the disrupters in 2020? Again, it was Sanders and Trump, certainly not Biden. Biden looks more and more like a placeholder for the Democratic liberal left.

The different voters’ responses of the Democratic left and Republican right to party dysfunction are worth noting. Leading up to the 2016 Republican primaries, Republican voters had already dismissed the Republican vanguard that failed to represent their interests. John Boehner, Eric Cantor, Jeb Bush, John Kasich, John McCain, Mitt Romney, all had been pushed to the sidelines by primary voters. On the Democrat side, despite the populist and popular criticisms by Bernie Sanders, nothing of the sort happened, as establishment Democrats were rewarded with re-election. The biggest surprise was probably the election of a few political novices, like Alexandria Ocasio-Cortez and Ilhan Omar, but they hardly represented the concerted voices of disaffected Democratic voters.

This dichotomy among partisan voters is likely driven by the behavioral predilections of right-leaning conservatives vs. left-leaning liberals. Conservatives believe in small, decentralized government and individualism, whereas liberals see centralization and collectivism as the solutions to national problems. It is much more difficult for the Republican party to get its voters to march in lockstep, while it comes rather naturally for liberal Democrats. There was almost no objection to the DNC sidelining Sanders, who proceeded to endorse his primary opponents Hillary Clinton and Joe Biden. On the other hand, Republican voters ended up going all in for the anti-establishment candidate who might disrupt ‘politics as usual.’ So, disruption is coming from only one side of the political aisle, while the other stands pat trying to hold onto power.

But if Trump is a symptom, then all the anti-Trump rhetoric is a dangerous sideshow. It maintains the illusory center of attention through the megaphones of the media and establishment political parties. But in no way am I able to condone removing our institutional constraints in order to delegitimize a presidential administration, no matter how much I disagree with the policies of that administration. But while institutional constraints have been applied in total against Trump’s indiscretions and miscues, there has been no institutional constraint on the anti-Trump side. This has led to a double-standard of justice that serves politics, not justice.

Like I said, all this craziness has convinced me that going back to the establishment of Clinton, Biden, Bush, Obama, McConnell, Schumer, and Boehner is a non-starter. I argued this reasoning for the re-election of Donald Trump in 2020. The J6 protest was another symptom of the disruptive forces in our politics. Trump was imprudent to stand pat when the protest turned riotous and he has suffered politically for that mistake ever since. It was not smart politics, as he seemed to be driven by his ego.

So let me be clear on what I’m arguing. The disruption we need is not to destroy the institutions of our democracy, but to replace the political class that is failing to uphold the interests of the voters it claims to represent. This means that incumbent politicians and their party apparatus need to be challenged by voters and I suspect most of this challenge is coming from the right. And their standard-bearer is, for better or worse, Donald Trump. While this might sound like an endorsement of Trump to those No-Trumpers out there, it’s really a decrying of the politics-as-usual status quo that seems to be dividing this nation into two camps. As they say, “Throw all the bums out!”

I find it ironic that the No-Trumpers are arguing that such populist rhetoric now threatens our democracy. (Yes, it seems only right populism is the threat, left populism is, well, the voice of the people?) But isn’t populism the distilled essence of democracy? But, they say, Hitler was elected by a democracy. Technically true, but the institutional constraints had collapsed and Hitler amassed an army of supporters under the Nazi Party with the SS and Gestapo. Trump has certainly not enjoyed any such support from the US military or the FBI or CIA. On the contrary, all these bureaucratic enforcement elites appear to have been vociferously opposed to POTUS Trump.

So, isn’t the real threat the politicization and corruption of our institutions? From what I see, Trump has been constrained by thousands, if not millions, of bureaucratic Lilliputians, while the institutions of the Justice Department, the FBI, the CIA, the military, and the Fourth Estate all seem to be doing the bidding of a political party. These institutions have worked for us in the past because they have not done the work of politics, but rather the work of the Constitution. If so disfavored, Trump, or Biden, or whoever, should be removed by the electoral process. To prevent this happening through fair elections is the real threat to democracy.

I don’t have a lot of hope for bridging our national politics coming up to 2024, because nothing is resolved. Biden offers a sclerotic and incompetent response and Trump a chaotic one. The Rich Men North of Richmond appear to be losing total control and the natives are restless. Perhaps it will take a crisis for disruption to really take hold. One can only wonder how it will all turn out. I don’t have the answer, but I do know one thing with almost complete certainty: Trump or No Trump? is not the question. Pray for a miracle.

Keyu Jin’s book, The New China Playbook, delves into a timely subject of great interest to those intrigued by geopolitics and the enigma of modern-day China. Emerging from the depths of Maoism and the communist Cultural Revolution, China has rapidly transformed into one of the world’s dominant economies within a single generation. Spanning over thirty years, from Deng Xiaoping’s reforms in 1978 to the second decade of the 21st century, China’s GDP surged at an astonishing annual rate of 10%. This growth has occurred under a unique combination of stringent political control and a relatively laissez-faire economic environment that defies facile categorization as purely socialist or capitalist. In this respect, one must conclude China’s experiment is a resounding success. Consequently, Jin’s exploration of Chinese culture, politics, and society offers a wealth of historical significance and analytical insights. Backed by extensive research and a flowing narrative, her goal is to rectify perceived misapprehensions harbored by her Western readership in order to foster mutual understanding.

In her endeavor to explain the New China to her Western audience, Jin consistently harks back to Chinese culture rooted in Confucianism and historical experience. In essence, the New China retains connections to Old China. A defining trait of Chinese cultural history, Jin posits, is its paternalistic character accompanied by a willing embrace of social conformity. This sums up the main theme of Jin’s narrative. The contrast with Western European and American emphasis on individualism and free expression is the hallmark of contemporary Chinese culture. One might argue that there exist three discernible cultural models characterizing modern societies: paternalism as practiced in China, maternalism embodied by European social democracies with their “nanny-state” approach, and the market-based, individualistic ethos of American culture.

Chinese paternalism appears primarily focused on maintaining social order, political stability, and economic security, with secondary consideration given to individual freedom of expression and privacy. Citing the World Values Survey, Jin points out that 93% of Chinese people prioritize security over freedom, while 72% of Americans prioritize freedom over security. She also notes that many Chinese have signed up for the voluntary social credit system for being a “good” (quotes mine) citizen, suggesting that material and social benefits of conformity outweigh the loss of privacy and freedom of choice.

Jin adeptly navigates the delicate balance between China’s achievements and its shortcomings, and the implications for the nation’s citizens. She blends generational pride and gentle constructive criticism while accepting the regime’s authoritarian stance. However, certain topics are conspicuously absent from her narrative. One might suspect the specter of government censorship and sanctions might have an effect on the willingness of Chinese nationals to speak directly on certain matters in the public realm, but self-censorship promotes this tendency to gloss over some of the Chinese Communist Party’s deficiencies, along with the hidden costs and challenges associated with its policies.

Conspicuously absent is any discussion of the personal costs of Mao’s one-child policy or the crackdown at Tiananmen Square in 1989. Additionally, the book discounts China’s trade mercantilism and its detrimental impact on export capacities and capital inflows for competing developing countries. The coercive incentives underlying China’s Belt and Road initiatives goes unrecognized. She fails to address China’s handling of the pandemic, the origins of the virus in Wuhan, and the roles of organizations like the WHO and the US NIH. The global costs of the lockdown policies adopted by various nations, in light of China’s approach, is an important postscript to failed pandemic policies.

Furthermore, there is no mention of China’s aspirations to establish a new international currency regime centered around the BRICS countries. The viability of such a reserve currency hinges on political and institutional trust, which is notably lacking for the authoritarian Chinese Communist regime. Jin also overlooks the subjects of state-sponsored cybercrime and surveillance, even as she suggests an ethical awakening among Chinese millennials. Most significantly, she omits any discussion of the One China policy and Taiwan’s future status.

While Jin’s focus on conciliatory topics for the betterment of international relations is understandable, these sources of tension cannot be readily dismissed. China’s ambitions for the future undoubtedly played, and will continue to play, a substantial role in these dynamics.

One essential issue highlighted by Jin pertains to the challenge of maintaining political and economic stability going forward. It deserves special emphasis because it is a critical challenge China shares with the rest of the world as well. The crux lies in the skewed distribution of material resources, which leads to widening wealth and income inequalities. As an economist, Jin recognizes the association between skewed distributions and rapid growth in fluid markets, as wealth tends to concentrate due to winner-take-all dynamics. In nature and economies, success breeds success. She then draws the connection between economic inequality and the rise of polarized societies, surging populism, and widespread dissatisfaction with governance structures.

Ironically, perhaps due to her orthodox economic background, Jin overlooks a solution inherent in her own analysis. She alludes to the underdevelopment of China’s financial markets, attributing it to government-directed growth that bypasses the domestic financial system. This has inhibited the development of deep and broad financial markets. Governments finance by borrowing, with debt finance and leverage. This contrasts with the private American equity-based financial system, which allows for broader sharing of risk and financial upside across all participants. She notes how “the disconnect between economic growth and the stock market returns means that individuals and households cannot consistently enjoy the fruits of the economy’s fast growth through its capital markets…” Well, there it is.

This contrast between debt and equity draws on basic finance theory: debt concentrates through leverage; equity diffuses through the sharing of risk and rewards to success. Over the past four decades, global central bank policies have exacerbated the concentration of risks and rewards through debt finance and subsidized credit. The 2008 Great Financial Crisis was a consequence of this approach, and subsequent responses, like Quantitative Easing and Zero Interest Rate Policies, have accelerated asset bubbles and inequality. The remedy, albeit painful, entails reversing these policies by recommitting to economic and financial fundamentals. Concomitantly, it’s imperative for citizens in a free society to engage in wealth creation beyond labor inputs. They must possess equity in economic production and actively manage the associated risks. Unmanageable risks should be addressed through public policy interventions. While not a novel idea (as exemplified by pension systems), widespread capital accumulation is often disregarded by those who gain from the status quo.

This insight brings us back to the ideological inquiry about China’s claim of achieving a distinctive hybrid of socialism and capitalism, as presented in the book’s subtitle. It’s reasonable to question this notion, considering that China’s remarkable success in the past few decades may have largely arisen as a corrective response to the preceding century of stagnation—a rebound and catch-up from a profoundly low point. Answers may be revealed more in psychological and metaphysical comparisons than economic or political analysis, with the analogy of parenthood serving as a useful lens.

Paternalism, akin to military discipline, is valuable for instilling order and efficiencies, yet risks stifling initiative and fostering dependency, unless individuals are prepared for independent thinking and action. This same criticism applies to maternalism. Nurture, by nature, should equip individuals with independence and self-reliance to enhance survival. In a society where citizens have the freedom to flourish or falter based on their efforts, embracing and effectively managing risk is essential for success.

Human success on the ground stems from self-discipline and self-confidence, individually and collectively. To put it succinctly, discipline is learned, while confidence is earned. Just as parents teach self-discipline to nurture self-confidence and self-respect in their offspring, societies must encourage citizens to participate in the wealth creation process through prudent risk-taking and risk-management. In this way, we adapt to change. In a world of risk and uncertainty, human progress is not advanced by the strongest or smartest, but the most adaptive. It remains to be seen if China’s model is as adaptive as the proven US model, despite its current difficulties.

In conclusion, it is noteworthy that these Western misconceptions about China Jin alludes to could partially arise from deliberate opacity cultivated by the Chinese government to control the dissemination of free information, diminish political accountability, and manage the actions and ambitions of its citizens. This layer of opacity will only inhibit foreigners’ understanding China’s complexities.

I recently watched a video interview posted on the Wealthion YT channel with a financial journalist. The discussion delved into a broad swath of societal ills and potential crises plaguing us, from elite leadership failures to inequality to Federal Reserve policy. You can view it here, but my comments below…

…a very broad interview that covered a lot of ground in a compact time frame. Perhaps a bit too ambitious? But I felt the discussion floundering around a bit on the frothy surface without getting down to the deeper undercurrents of our societal situation. I have a few comments to try to integrate those undercurrents.

First, modern society has grown more complex. The political response to this increasing system complexity has been to centralize control, especially in the Federal government and bureaucracy. This is exactly the wrong approach. Complex systems are best managed through the decentralization of decision-making with high-level coordination. That’s why we have 50 states and 3200+ counties. Democracy is decentralized. A free society is decentralized, so the problem of leadership in a complex system is trying to do the impossible and failing. This is one part of our crisis of leadership.

Next, the more disconcerting crisis is likely due to the slow degeneration of cultural values. Both of you are probably too young to feel the change that happened in the 60s with the babyboom generation. The shift was from the self-sacrifice of the Greatest Generation that lived through the wars and depression and their offspring that fought in WWII and Korea. The babyboom generation that followed was all about breaking conventions and responsibilities and shaping a new society in their image. Unfortunately, that image was half-baked and led to subsequent “Me” generations that eschewed the responsibilities of community and sacrifice. Babyboomers have taught subsequent generations all the wrong values – do the right thing to serve yourself and feel good about spreading that gospel. As a result, religion and church were discarded, communities became atomized, and the rise of secularism led to no common reference point. It was all about “me and my feelings” and social justice was about what somebody else should do. We have become tribal. This has poisoned our leadership cadre across the political world, the corporate world, entertainment, sports, etc. It seemed that there are no public heroes anymore while we worship the lifestyles of the rich and famous.

This attitude toward social values has led to every man (and woman) for themselves and justifies all kinds of narrow anti-social behavior. It’s narcissistic nihilism. Gordon Gecko’s “Greed is good” was wrong because greed is a negative social value. In a free society “self-interest” is good because it is neutral in terms of social value. It is self-interested to be altruistic, but greediness is not. These words have meanings.

The breakdown in cultural values permeates our leadership to where it seems acceptable for CEOs to earn 800 times their low-level employees. It justifies politicians front-running the stock market before legislation that gives them inside information. It justifies deceitfulness in the media to spread a desired narrative. It pretends that multiculturalism means non-assimilation. In the end, it destroys trust in the institutions that support a free society. I do believe correcting cultural degeneration requires a social crisis and a turning of generations. The Fourth Turning?

Charles Hugh Smith’s framework is useful but I think misinterpreted because it fails to distinguish between reality and wishfulness. The public may wish for free healthcare for all, an end to poverty and hunger, UBI, an EV in every garage, but that doesn’t square with economic reality and politicians can’t deliver such fantasies. The reality is that economic markets impose constraints, so we are in a ‘box’ and politics is about choices we can make within that box; trade-offs if you will. Some choices may help expand the box, but we can’t just jump outside the box like Bernie would like. Socialism is an attempt to jump outside the box and always fails. Capitalism at least grapples with reality, even if we don’t like it.

Finally, this brings us to trying to understand our economic forces today. The discussion here turned to notions of inequality and economic injustice that seem very elusive to the average observer. I think economic inequality needs to be understood in the context of what are called power laws, or Pareto laws or 80-20, also called winner-take-all dynamics. We observe these dynamics in nature, where 20% of the pea pods yield 80% of the peas. Success breeds more success. This applies to economic dynamics as well. Finance exhibits centripetal forces where the value gets sucked up by the center and leaves the periphery starved. Technology and fintech amplify these dynamics on steroids. The secret to understanding inequality in market capitalism is to realize that capitalism concentrates ownership and control, especially of capital. This fact disturbs laborites, but the end goal of capitalism is not more, higher-paying jobs – it’s the exact opposite. The end goal is the accumulation of productive capital. Labor in this system does not primarily create wealth, it mostly distributes wealth. Poorly because successful capitalism decreases input costs to increase the profits of success. Our policy focus on labor is an anachronism of the industrial age. That may be a very controversial statement but the theoretical dynamics of economics confirms it. If your income is based solely on wages, you’re on the wrong side of the profit equation.

Designing policy to tilt capitalism toward labor incomes is self-defeating; the real solution lies in making sure every citizen participates in capitalism as a residual claimant. In other words, I want to participate as a risk-taking capitalist with equity who then reaps the rewards of success. This is best accomplished in a society that promotes risk-taking through decentralized markets. No, we do not want Jamie Dimon controlling the banking credit system, no matter how benevolent he may be (JPM always seems to get sweetheart deals at the expense of somebody else’s shareholders, yes?). A free society demands decentralization of value creation and decentralization of the returns to value. Many of our financial and tax policies mitigate against decentralization of finance. It’s the old saw about the bank will only lend to borrowers who don’t need the money. When we understand the dynamics of ownership and control in the context of uncertainty and risk-taking, we can assess policies that yield positive results for the greatest number vs those that yield ever-concentrated forms of ownership and control.

For example:

1. Debt concentrates risk, equity spreads and diversifies risk;

2. Private equity concentrates ownership, control, and returns; public stock markets diversify risks and returns;

3. Small businesses enhance freedom; large corps promote serfdom;

4. Entrepreneurship promotes freedom; UBI promotes serfdom;

5. Charitable foundations concentrate control over resources; wide distribution of capital promotes innovation and returns to value creation;

6. Competition promotes efficiency and economic justice; monopoly promotes exploitation and inefficiency;

7. Concentrated political power leads to corruption, inefficiency, and injustice; political competition and transparency leads to economic efficiency and social justice;

8. A competitive, open, transparent market is the best regulator of human behavior ever invented. One must be free to succeed AND fail;

9. Diversified asset portfolios offer the most efficient and safe means to manage risk in a world of uncertainty;

10. The goal of public policy is to promote liberty and justice through anti-fragility, not-God help us-fairness.

11. He (or she) who bears the risk, reaps the reward – this is moral justice.

One gets the idea, which is to manage risk to create robustness and adaptability to uncertain contingencies…anti-fragile, in the words of Nassim Taleb’s book with that title.

I reprint here an article written by Ken Fisher on markets and the banking industry published in the NY Post.

Why fears of a banking crisis were overblown — bad regulation is the real problem

Ken Fisher May 21, 2023

Is there really some banking crisis?

In March, I told you Silicon Valley and Signature Bank were isolated episodes—not systemic threats.

First Republic’s subsequent demise and plunging regional bank stocks furthered fears of an imploding domino effect. Yet these episodes and emerging data reinforce my point. Contagion isn’t the risk now, potential bad regulation is. Hear me out.

Hoopla aside, since SVB’s failure, the S&P 500 is up 6.5%.

Yes, regional bank stocks are down. But larger S&P 500 Financials are off just -1.6% since SVB’s collapse. Overall bank deposits are down -2.5% — smaller banks’ -4.6%. Not great but not catastrophic, either. And lending hasn’t imploded. The Fed’s Q1 Senior Loan Officer Opinion Survey showed slightly tighter lending standards and lower demand — neither new nor severe.

I had argued SVB and Signature chiefly failed from hyper-concentrated deposit bases — the former in Venture Capital, the latter in cryptocurrency.

Few banks are so concentrated with such mutually communicative depositors.

Tightly knit depositor communities make bank runs easier.

FRC was somewhat similar, courting wealthy clients that were geographically and culturally overlapped with SVB’s — pushing specialized products with uncommonly high uninsured deposits.

Depositors fearfully yanked savings, the stock imploded, and fearing total failure the FDIC interceded, took control and brokered a near failure, sweetheart takeover by JPMorgan on May 1.

Yet no calamity ensued. Why? Inflation adjusted, these few banks weren’t huge. Just the clucking was. Second tier and smaller banks fail regularly — averaging 63 per year since 1975. They often collapse in clumps, like 1989 — 1990’s 912 or 2007 — 2008’s 305. The only years with none? 2021 and 2022!

But now we notice. Hyping these few confuses exceptions with the norm. The overall system is near its healthiest in 10, 30 or 50 years based on loan-to-deposit ratios and cash relative to total assets.

There are 4,200-plus US banks. We want a vibrant, dynamic capitalist economy — including innovative banks. With that comes some failing, always. We should want that. Regulators try to ring-fence risk. They can’t fully. And shouldn’t.

When banks need emergency liquidity, they first borrow from their regional Federal Reserve District. There are 12 nationally. Those regional loans are reported weekly. Only the New York District (Signature’s home) and the San Francisco District (SVB and FRC) saw upticks.

The other 10? Nada! In any systemic crisis, that borrowing would be widespread, everywhere.

You say regulators should have “done something” before all this? Really? Be careful what you wish for. Throughout government there is almost no actual inside-banking, real world, work experience. Treasury Secretary Yellen was just a pinhead academic economist who, ironically, ran the now-maligned San Francisco Fed District where all these SVB/FRC issues spawned — before becoming Fed Chair.

Incompetence promoted!

Current Fed Chair Jerome Powell is a born-and-bred DC lawyer, politico, swamp critter with zero real banking experience. Pretty much all are.

Congress? Worse! A lot of smart lawyers on relevant committees. I know and like lots of them but can count on one finger anyone senior in actually running any bank ever — Rep. French Hill (R-Ark.).

But they itch to “do something.” Anything they do is likely worse than nothing — because they know nothing. Altered banking rules routinely backfire.

Calls for smarty-pants “fixes” to this non-crisis are why the SLOOS survey shows many banks now tightening credit — citing, “concerns about … future legislative changes.” Congressional banking inaction beats reaction. Less is more. Doing nothing is best. Republicans should get that cold but, seemingly, don’t. So far, most regulation talk is abstract politicking. If that holds, bank fears will fade faster than this column’s ending.

My comment:

“SVB and Signature chiefly failed from hyper-concentrated deposit bases — the former in Venture Capital, the latter in cryptocurrency.”

This is the key takeaway from our recurring financial crises. Concentration of ownership and control through debt leverage has made our financial system, economy, and our society far more fragile and susceptible to uncertainty and risk. This is what caused the contagion of the GFC through securitization of MBSs and recapitalization through interest rate suppression, thereby losing the independence of diversified asset markets. When all asset markets move as one, there is no place to hide – kind of like going down with the Titanic.

Risk management is the key to financial stability through policymaking. It is ignored by our politicians, and exploited by the financial elites seeking to privatize gains and socialize losses.

From Jesse Felder’s Felder Report. More results of the Fed’s reckless monetary policy under Bernanke. This guy goes down in infamy.

——————–

It’s no secret that for the past decade and a half the Federal Reserve has made it its mission to create a “wealth effect” in the economy by boosting asset prices. Back in 2010, Ben Bernanke explained, “…higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.” And so he began a process of printing money with the explicit purpose of inflating asset prices, a policy that has been continued by each of his successors.

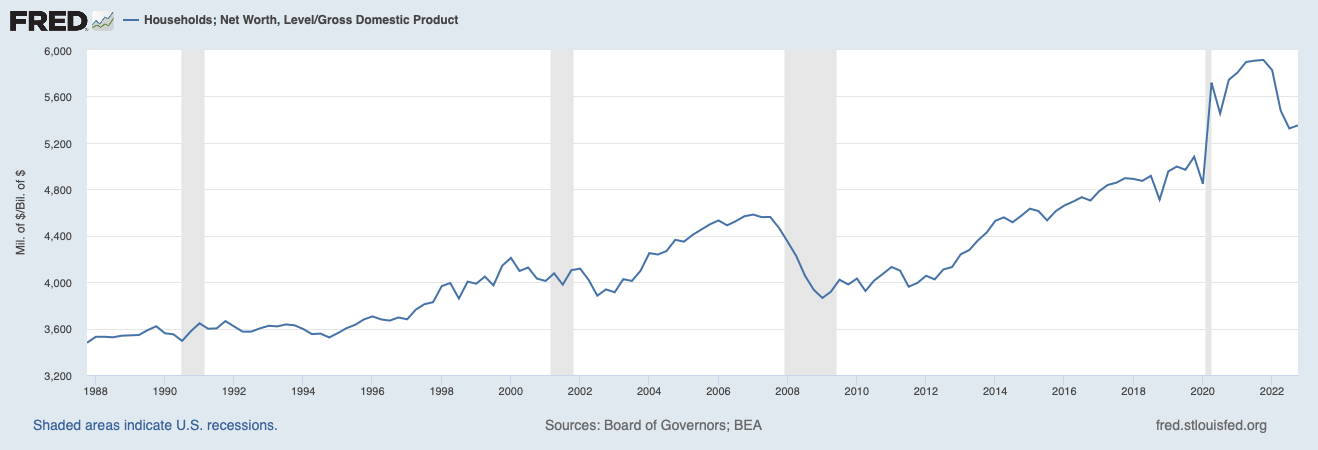

Over this time, quantitative easing, as the policy is called, has been inordinately successful in boosting asset prices while not so effective in boosting the economy. The most straightforward evidence of this is the fact that household net worth relative to the economy has soared to record highs during the QE era. If it had worked the way Bernanke intended then, after a brief surge in the ratio, it would have flattened out as growth in the economy caught up to growth in asset prices. Clearly, that didn’t happen.

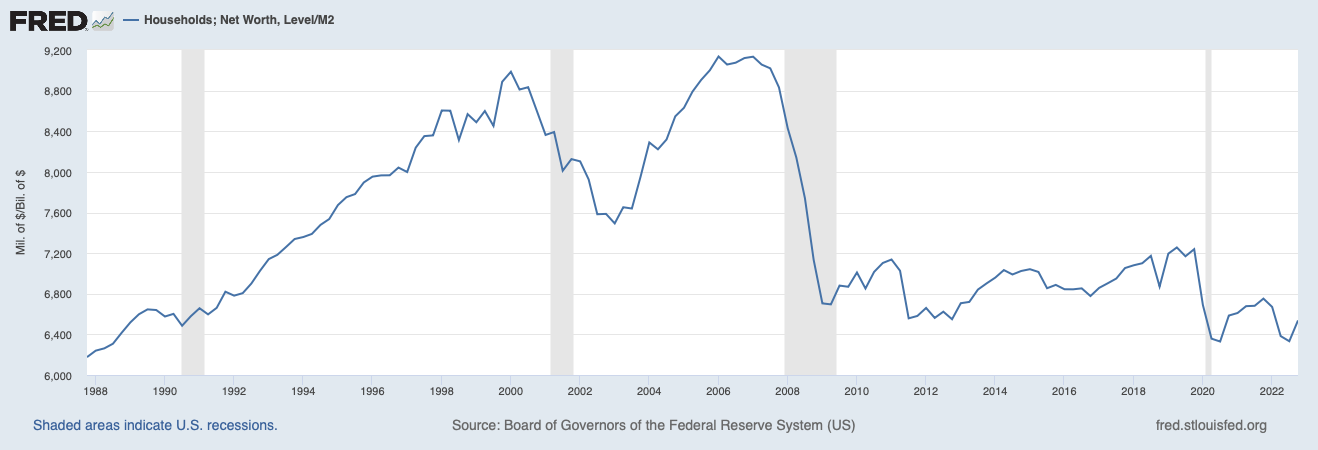

It does appear, however, as if the central bank did at least accomplish the first half of Bernanke’s mission (boosting wealth) even if it didn’t quite accomplish the second half (kickstarting a virtuous circle of economic growth). But when you look at household net worth relative to the growth in the money supply, it’s clear that the rise in the former was nothing more than an illusion. Net worth has actually declined relative to M2 since 2008 and is now back to levels not seen in the 20 years prior to that time. The truth is that there has been no “real” wealth created at all when measured this way.

And when you deflate GDP by the growth in the money supply, the picture is even more damning. Since quantitative easing began in 2008, the trajectory of the economy in relation to the growth of M2 has been far more deeply negative than that in household net worth. The truth is that there has been no “real” growth in the economy since 2008 when it is measured in this way; in fact, the economy has been in protracted decline relative to the money supply for decades, a phenomenon that has only worsened during the QE era.

As today’s CPI report reminds us, that after decades of disinflation the most recent round of money printing has lead to the return of inflation. At the end of the day, it may not be the economy or household net worth but inflation that the central bank’s great monetary experiment has been most effective in stoking. Of course, history could have told us that would be the likely outcome long before Bernanke ever began firing up the printing press. And it’s failure to heed the warnings of history may help to explain why confidence in the Fed is now at an all-time low, a trend that may only exacerbate the inflation problem over time.

The irony was palpable. An interview with a Federal Reserve Bank official from last fall, claiming that “we’re a long, long way from any kind of disruption” to the financial system — followed in short order by television clips showing the failure of Silicon Valley Bank.

But as “Age of Easy Money” shows, the recent bailout of Silicon Valley Bank represents only the latest example of the Fed disrupting the economy and banking system — almost always with long-term consequences.

A documentary, two years in the making, but chronicling 30 years of monetary and fiscal mismanagement. Something we’ve been chronicling here for the past 15 years…

And here’s the most recent fiscal mismanagement. The Biden administration’s $6 – $7.6 TRILLION spending shock:

The $1.9T American Rescue Plan projected to realistically involve $3.5T in spending

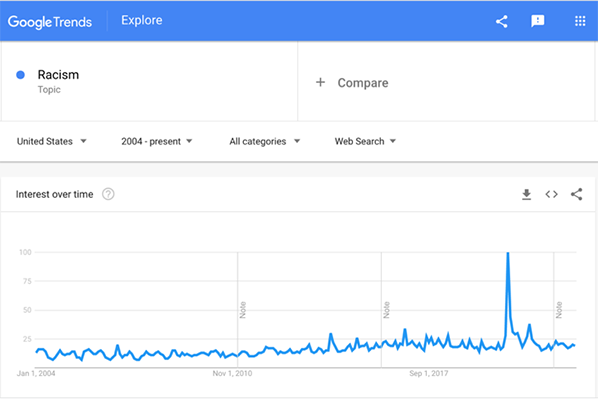

Racial divisions have become the stalking horse of our politics and social discourse, with racism defined as white on black (often extending to Western vs. non-Western ethnicities). Google Trends reveals how the online topic of racism has steadily risen over the past decade, spiking like a seismic reading of an earthquake in June, 2020 that marked the George Floyd tragedy and the Black Lives Matter protests that followed.In due course we’ve been treated to a surfeit of acronyms to help us understand our racial divisions, from BLM and CRT to DEI, CSJ, and SEL.1

Our educational institutions have done their best to promote race consciousness in schools through books and pedagogic exercises defined by racial groupings. One teachers’ handbook promises to “equip students to engage with the most urgent issues of our time. With a groundbreaking intersectional approach framed around social spheres, Race in America gives students the tools to think critically about race, racism, and white privilege.”

This is not so much about learning history as promoting tribalism. The standing premise is that race dominates all identity classifications for explaining disparities among groups.Certainly, anecdotal and systemic racism has played its part, but then again, unresolved debates over preferences, crime, constitutional challenges to Affirmative Action, self-segregation, and voting rights raise questions over whether the emphasis on race and its root in identity politics has advanced the cause of racial equality or has even been the determining factor of political, social, and economic outcomes.

After a century of post-bellum struggles and breakthroughs during the civil rights era, it would appear we are now moving farther away from the ideal of Martin Luther King Jr.’s dream of a color-blind society.The current Supreme Court case on redistricting in Alabama under the Voting Rights Act of 1965 is an illustrative case. The VRA was instituted as part of the defense of civil rights to protect the right to vote for minority groups by prohibiting race as the basis of electoral rules. We see the unintended result in gerrymandered minority districts that create higher shares of black voters electing black representatives. But this not only violates the spirit of the VRA, it promotes self-segregation, creating the separation of races the policy is seeking to integrate.

In two other SCOTUS cases, a student advocate group is suing Harvard University and the University of North Carolina over race-based admissions policies. And most recently, the scandal involving racial and ethnic battles on the Los Angeles City Council has exposed the fragility of a race-based political coalition based on a unified community of “persons of color.”

The underlying assumption that DNA determines outcomes is at the heart of the problem. It assumes that group interests can only be justly represented by members of that same identity group and all groups must be represented in proportion to their share of the population. Anything less is racist. So, blacks must elect black representatives, Hispanics for Hispanics, Asians for Asians, etc. If our goal is integration and assimilation to achieve race-blind outcomes, this trend inevitably sets us back.

Why Race?

We should accept that the issue of race in America is confounded by the historical legacy of the African slave trade. Such anti-black racism was institutionalized for much of our history with slavery followed by Jim Crow laws and forced segregation up until the 1960s. In more recent times we have witnessed highly publicized racial altercations with law enforcement associated with the Rodney King, OJ Simpson, Trayvon Martin, Michael Brown, Breonna Taylor incidents. We hit the tipping point with the tragic case of George Floyd.

We cannot dismiss such shocking events, but the boiling outrage obscures how infrequently such racist acts occur in today’s America. So infrequently that some racialists feel the need to create them. In his book, Hate Crime Hoax, Wilfred Reilly (a black scholar) documents a dataset of 409 allegedly false or dubious hate crime allegations (concentrated during the past five years), which he describes as hoaxes on the basis of reports in mainstream national or regional news sources. These hoaxes attempt to bolster the indefensible racist narrative.

Undeterred by the evidence, racialists have shifted focus in recent years from explicit racism to incontestable systemic racism. Their logic now argues that mathematics and science are racist. Time management is racist. Speaking grammatically correct English is racist. Wearing a tie is racist. We have gone from proving discrimination through legal means to suggesting disparate outcomes have racist causes (which is social science in reverse). This permits racialists not only to condemn oppressors who don’t even know they are oppressors, but also allows them to pose as virtuous, anti-racist, social justice warriors.2 After electing Barack Obama in 2008 and again in 2012, this reversal in race relations has taken most Americans by surprise.

Culture and Multiculturalism

During and after the civil rights movement there was a radical shift in urban black communities that promoted a unique American black culture that rejected those attributes of the “white” mainstream. This was marked by the split between MLK Jr. and Malcolm X, followed by the Black Panthers and Nation of Islam.

One problem with the “Afro-centric” formulation is that capitalism—in Asia, Africa or the Middle East—rewards and reinforces cultural behaviors that Max Weber labelled as the (European) Protestant Work Ethic. The key dynamic in capitalism is wealth building through capital accumulation that results from saving and investing in both financial and human capital (education). A culture or subculture that eschews saving and investing while encouraging over-consumption cannot benefit from the virtuous cycle of compounding wealth. Though pejoratively labelled “acting white,” these formulas for success are not racial or ethnic, they are cultural and can be adopted by any individual or population. The Jewish diaspora has long embraced these cultural attributes in response to their own segregation from Christian Europe. Admittedly, parsimony is not a virtue promoted by a market system pushing conspicuous consumption as a symbol for status and meaning.

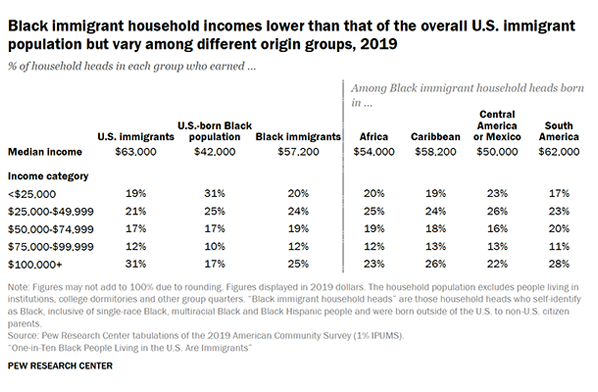

South Asian immigrants, of every shade of skin color, are another example: after barely two generations, South Asians as a group have the highest household median income in the US, followed by Taiwanese and Filipinos. One can make a distinction for African heritage, but black immigrant groups from Africa and the Americas also outperform in educational achievement, employment, and household incomes.3 In the past many American blacks were prohibited from accumulating capital and real assets under the systemic racism of the past, so they have been disadvantaged generationally. This can explain some of the racial disparity in wealth accumulation and why racial wealth gaps are far greater than income gaps. But the solution is not decrying racism of the past, rather we should adopt the dominant cultural formula for success regardless of race, creed, gender, or ethnicity.

Today’s racial narrative is often labeled cultural Marxism or racial Marxism. Marxist ideology is based on class divisions between capital and labor. Unfortunately for Marxist ideologues, class divisions have so far failed to solidify durable political coalitions in the US, even during the depression era. Americans see themselves as upwardly mobile, so class warfare has never been widely embraced.

In contrast, identity and especially race have proven far more potent as a political wedge necessary to a kind of faux “Marxist” agenda, particularly in the ideological hothouses of the media and the University. Rather than the class struggle, culture wars have come to define US political divisions since the 1970s and the purpose is disruptive. Today, the racist narrative has sadly become the most powerful identity marker because in political context, anti-racism is power. But this power play only serves to obscure the true dynamics of our political and economic divides.

The True Divide: Class

When we unpack inequality in the constellation of political and economic power, class division between capital and labor has historically been the most significant factor. Marx was correct (as he noted in Das Kapital, updated by Thomas Piketty with Capital), that capital concentrates success, while the market dynamic to maximize profits often depresses wage incomes relative to capital incomes. The capitalist principle that “money makes money” drives a wedge between those who have it and those who do not, creating our American class tensions between rich, middle class, and poor. This wedge has been widening persistently with the financial and fiscal policies of recent decades dangerously hollowing out the middle class.

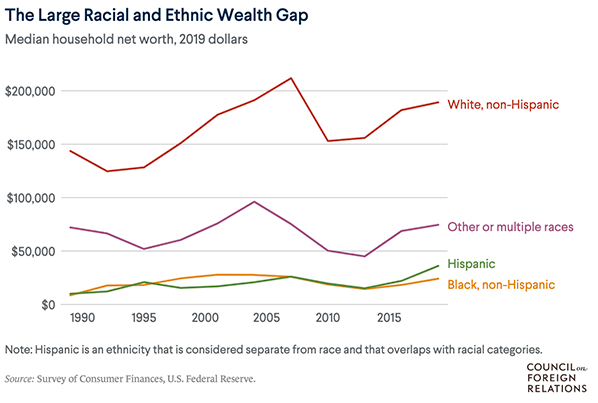

Pew Research data show that the richest families in the U.S. have experienced greater gains in wealth than other families in recent decades, a trend that reinforces the growing concentration of financial resources at the top.4 Another study by the Council on Foreign Relations notes that in 2021, the top 10 percent of Americans held nearly 70 percent of U.S. wealth, up from about 61 percent at the end of 1989.5 The share held by the next 40 percent fell correspondingly over that period. The bottom 50 percent (roughly sixty-three million families) owned about 2.5 percent of wealth in 2021. This widening of the wealth gap has roiled our national politics may be seen as disproportionately impactful on particular races, but exists as well within racial groups. There are rich blacks, and poor Asians and Jews, while, in sheer numbers there are more white people living in poverty than any other group.6

We certainly cannot absolve slavery and racism. As previously stated, American blacks and other poor minority groups have been historically disadvantaged from accumulating capital assets. That fact explains much of the differences between income and wealth disparities, holding other significant factors such as education constant. But in searching for solutions we need to keep in mind that chattel slavery as practiced in the pre-bellum South was as much about property and forced labor as a means of production on plantations as it was about the racial identity of the slaves. In material terms, slavery was an economic class phenomenon.

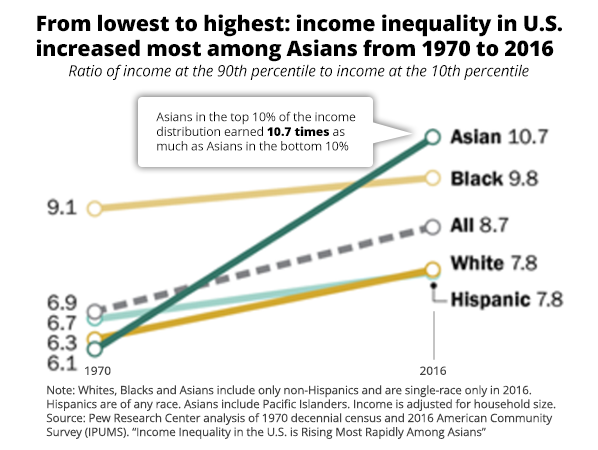

Further evidence that racism is not the primary driver of inequality in today’s America is illustrated by the experience of Asian immigrants and by the changes in income inequality over time within racial groups, especially among Asians. The median net worth of Asian Americans in 2019 was $156,000, placing them close to that of native white Americans.7 But the accompanying data from Pew Research shows that over the past 45 years growing inequality among Asians far outpaces other groups and that inequality among blacks is higher and rising faster than both whites and Hispanics.8 Racism cannot explain these trends within groups.9

A Cultural Correction

If we want to address the critical issue of economic inequality, the solution must be found elsewhere than in race and identity politics. In other words, it’s not about who you are as much as about what you do.

The widespread accusations of racist policing can help illustrate divergent cultural norms among minorities, especially for young black males. It starts with the breakdown of two-parent families under the well-meaning welfare policies of the Great Society programs. Economist Thomas Sowell has done excellent research documenting the disintegration of black families after the 1960s.This problem has been compounded by the decline in public school education under the urban political machine that has repurposed resources in response to political pressures, mostly from public unions. Without strong parental role models and inadequate educational opportunities, young urban minorities face few lucrative employment or career prospects, so where else to turn except to the highly lucrative drug trade? When the violent criminality of the drug trade becomes a political liability, the same urban political machine turns to law enforcement and the criminal justice system to solve the problem. Naturally this leads to far more direct altercations between police and urban minority males, increasing the inevitability of highly publicized human tragedies (these incidents harm victims and police, as well as alleged perpetrators). The thread of causation from poor, broken families to educational disadvantages to underemployment to criminal activity to police confrontations to unintended tragedies is fairly straightforward. We won’t fix anything for urban minorities if we don’t break this vicious spiral.

Furthermore, mischaracterizing our inequality as primarily racist has been bundled up with a stew of “woke-ism” that uses race and gender as the chosen identity markers rather than trying to create new, and broader, access to economic opportunity and advancement.

As Rev. King preached, we will need to get beyond race to discover who we are as a human community. The recent racial and cultural trend toward tribalism in Western societies is a step backwards and is not going to bring us to the Promised Land.